CFPB Releases New Consumer Complaint Data

In connection with the CFPB’s March 28, 2013 Consumer Response Field Hearing in Des Moines, Iowa, the Bureau announced that it would be making publicly accessible new consumer complaint data from mortgages, bank accounts, private student loans, and car loans in addition to credit card complaints that the Bureau has been making publicly accessible since Summer 2012. The CFPB expects the number of complaints made publicly available to expand five-fold from about 19,000 to potentially 90,000, and according to Director Cordray, the expansion represents the “largest collection of complaint data on federal consumer financial products and services ever made public.”

How Complaints Are Received

The CFPB Consumer Response Team screens all complaints submitted by consumers based on several criteria:

- Whether the complaint falls within the CFPB’s primary enforcement authority;

- Whether the complaint is complete; and

- Whether the complaint is a duplicate of a prior submission by the same consumer.

Screened complaints then are forwarded via a secure web portal to the appropriate company. The company reviews the information, communicates with the consumer, as needed, and determines what action to take in response. The company then reports back to the consumer and the CFPB via the secure “company portal.” The CFPB then invites the consumer to review the response and provide feedback.

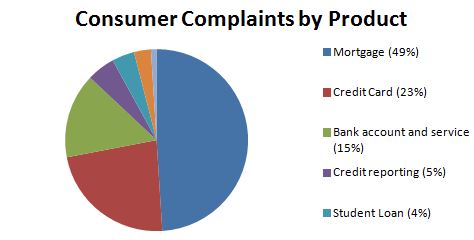

Types of Complaints

The following chart reflects the types of complaints received from July 21, 2011 through February 28, 2013:

Each consumer financial product contained complaints about various issues. The most prevalent issues for each product are as follows:

- Credit Cards: billing disputes and interest rates;

- Mortgages: problems consumers face when they are unable to make payments, such as issues related to loan modifications, collections, or foreclosures;

- Bank accounts and service: opening, closing, or managing the account;

- Private student loans: repaying the loan, such as fees, billing, deferment, forbearance, fraud, and credit reporting;

- Consumer loans: managing the loan, lease, or line of credit; and

- Credit reporting: incorrect information appearing on the consumer’s credit report, such as information that is not the consumer’s, incorrect account status, and incorrect personal information.

Implications

Consumer complaints provide the CFPB and other federal and state regulators access to data that could become the subject of CFPB supervisory activity or enforcement actions. In his prepared remarks on March 28, 2013, in Des Moines, Director Cordray made clear that consumer complaints would provide “a source of information that [the CFPB would] consult in approaching our supervisory work” and “leads for our enforcement work of investigating and addressing potential wrongdoing.” Given the potentially prominent role that complaints will play in informing the CFPB’s work going forward, covered entities should ensure that they have access to the CFPB’s Company Portal in order to view and respond to consumer complaints and have the proper policies in place internally to address the sources of consumer complaints.

The CFPB will continue to make available complaints submitted through both the Portal and the FTC’s Consumer Sentinel complaint database to other federal regulators and state law enforcement -- including state attorneys general. This represents historic horizontal and vertical information sharing across regulators which could support more robust enforcement actions from state and federal regulators.

As part of the CFPB’s “open-data agenda”, expanded public access to the Portal will provide the public and consumer protection advocates with access to real-time consumer complaint data likely increasing covered entities’ litigation risks and the likelihood of adverse media coverage.

What Now?

It is clear that the end game for the CFPB in expanding the public’s access to consumer complaints is to create heightened marketplace and regulatory scrutiny of consumer financial service providers. As the Bureau looks to expand the public’s access to consumer complaints, covered entities and potentially covered entities should begin the process of preparing themselves for investigations, CFPB supervision and enforcement actions that could arise out of recurring consumer complaints.

The implication from the CFPB is that going forward, monitoring and responding to consumer complaints submitted to the Portal should become a part of every covered entity’s compliance regime. The CFPB is sending the message that firms should ensure that their consumer complaint and dispute resolution policies are appropriately scaled to the volume of consumer complaints, and that firms should analyze “root-causes” of complaints to understand systemic compliance issues.

About Troutman Sanders

Troutman Sanders is an accomplished and experienced leader in providing litigation and regulatory advice to a broad spectrum of financial services institutions, including mortgage originators and servicers, financial institutions and nonbank entities whose consumer complaints are now subject to public disclosure as a result of the CFPB’s decision to expand public access to the Portal. Troutman Sanders’ CFPB Team monitors the development and activities of the CFPB on its CFPB Report blog, advises clients on CFPB and Dodd-Frank issues and also provides compliance audits for consumer financial service providers regulated by the CFPB. Additionally, Troutman Sanders’ State Attorneys General practice group has successfully represented consumer finance service providers responding to attorney general investigations.

© TROUTMAN SANDERS LLP. ADVERTISING MATERIAL. These materials are to inform you of developments that may affect your business and are not to be considered legal advice, nor do they create a lawyer-client relationship. Information on previous case results does not guarantee a similar future result.