SEC Still Observing Deficiencies Involving Private Fund Fees and Expenses and Conflicts Disclosure

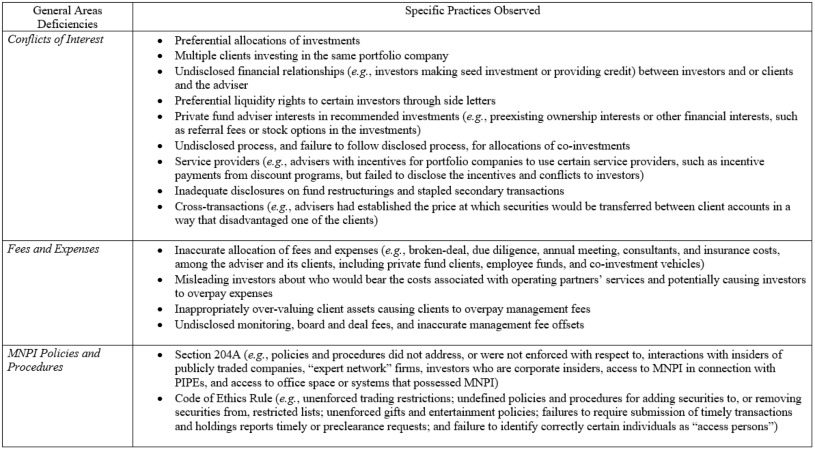

On June 23, 2020, the SEC’s Office of Compliance Inspections and Examinations (OCIE) issued a risk alert highlighting the following three general areas of deficiencies OCIE identified in examinations of private fund advisers: (1) conflicts of interest, (2) fees and expenses, and (3) policies and procedures relating to material nonpublic information (MNPI). OCIE hopes this latest risk alert will assist private fund advisers in reviewing and enhancing their compliance programs, and also will provide investors with information concerning private fund adviser deficiencies.

Déjà vu?

This is not the first OCIE guidance reminding private fund managers to review their policies and procedures to avoid these types of deficiencies. Shortly after the initial round of exams following the Dodd-Frank wave of private fund manager registrations in 2012, OCIE observed a high rate of deficiencies involving private fund manager fees and expense allocations. Since 2015, OCIE has often included in its annual exam priorities roster private fund fees and expenses, disclosure of conflicts of interest, as well as actions that appear to benefit the adviser at the expense of investors. [1]

The SEC followed through on its exam priorities. The SEC has initiated multiple actions against private fund managers since 2015 on violations such as expense allocation, undisclosed fees, and undisclosed conflicts of interest, including with respect to broken deal expenses, accelerated monitoring fees, and affiliated consulting fees. [2]

OCIE has similarly reminded advisers to review compliance programs for MNPI deficiencies. In February 2017, OCIE published a risk alert listing the five most frequent compliance topics identified on investment adviser examinations completed within the past two years — Code of Ethics rule violations made the list. Representative violations of the Code of Ethics Rule centered on the advisers’ failure to satisfactorily provide information about the advisers’ codes of ethics. Among other things, the staff observed that advisers failed to comprehensively identify their “access persons,” neglected to timely disclose information pertaining to holdings and transactions reports, and failed to properly describe their codes of ethics in Form ADV filings.

Again, on April 12, 2018, OCIE released a risk alert identifying the most frequently cited compliance deficiencies relating to fees and expenses charged by SEC-registered investment advisers to their clients. In particular, the 2018 risk alert highlighted OCIE’s observation of fund managers misallocating marketing expenses, regulatory filing fees, and travel expenses to fund clients instead of the adviser, in contravention of the applicable advisory agreements, operating agreements, or other disclosures. OCIE’s stated objectives in issuing the risk alert were to encourage advisers to assess their advisory fee and expense practices and related disclosures to ensure that they are complying with the Investment Advisers Act, the relevant rules, and their fiduciary duty, and review the adequacy and effectiveness of their compliance programs.

We have already observed recent private fund exam document request letters lasering in on these issues and anticipate more to come. If history has its way and repeats itself, we may be in store for another round of private fund enforcement actions related to expense allocation, undisclosed fees, and undisclosed conflicts of interest.

Compliance Takeaways

Private fund managers should take heed of OCIE’s guidance and assess their advisory fee and expense practices, related disclosures, and MNPI policies and procedures. In particular, firms should consider the following takeaway tips for reviewing these compliance matters:

- Review your firm’s current compliance policies and procedures to confirm consistency with the terms of your fund governing documents and Form ADV disclosure.

- Review your general ledgers to confirm expenses have been properly allocated as between the adviser and the funds you advise. A best practice is to have the fund governing documents expressly enumerate the line items allocated to the fund.

- Periodically test to confirm the fees charged were properly calculated and the expenses allocated to the fund were authorized under the fund documents.

- Review breach logs to ensure any detected violations are remediated and procedures updated to prevent future violations.

- Confirm your fund investors are on the same page as you about fund fees and expenses (particularly any management fee based on values) by making periodic disclosures to your LPAC/investors about the fees and expenses paid by the fund.

- Check out our recent client advisory discussing the “Do’s and Don’ts” of insider trading/MNPI issues while working from home.

For more information on private fund fees and expenses, please check out this podcast on fund fees and expense trends, as well as the article “ Fund Fees and Expenses-A Tale of Four Surveys: Trends 2014-2018”, from Julia D. Corelli of Pepper Hamilton. The field surveys for the 2020 Fees and Expenses Benchmarking Survey sponsored by Pepper Hamilton, Private Equity International, Withum, and PEF Services are complete and the results will be released in the fall. Please email Brian Dolan (dolanb@pepperlaw.com) if you want to receive the results once they are available.

[1] See, http://www.sec.gov/about/offices/ocie/national-examination-program-priorities-2015.pdf; https://www.sec.gov/about/offices/ocie/national-examination-program-priorities-2016.pdf; and https://www.sec.gov/about/offices/ocie/national-examination-program-priorities-2017.pdf.

[2] See, http://www.sec.gov/litigation/admin/2016/ia-4493.pdf; http://www.sec.gov/litigation/admin/2015/ia-4219.pdf; http://www.sec.gov/litigation/admin/2015/ia-4131.pdf; http://www.sec.gov/litigation/admin/2015/ia-4253.pdf; https://www.sec.gov/litigation/admin/2018/ia-5079.pdf; https://www.sec.gov/litigation/admin/2016/ia-4529.pdf; http://www.sec.gov/litigation/admin/2014/ia-3927.pdf; http://www.sec.gov/litigation/admin/2016/ia-4494.pdf; http://www.sec.gov/litigation/admin/2015/34-74828.pdf; http://www.sec.gov/litigation/admin/2014/33-9551.pdf; https://www.sec.gov/litigation/admin/2015/ia-4258.pdf and https://www.sec.gov/litigation/admin/2020/ia-5485.pdf.