“Mega Roth” – A Tool to Maximize Tax-Free Earnings with In-plan Roth Conversions of After-tax Contributions

Are your executive team members interested in increasing their savings to your company 401(k) plan? If so, consider amending your plan to include a “Mega Roth” feature – an in-plan Roth conversion of after-tax contributions in the year they are made to your defined contribution plan (the “DC Plan”). This strategy converts taxable earnings on after-tax contributions to tax-free earnings and can be a windfall for long-term savers.

How does an In-Plan Roth Conversion Work?

First, participants contribute pre-tax and/or Roth contributions to the DC Plan up to the limit ($19,000 in 2019; $25,000 for participants over age 50) and receive any employer matching and/or non-elective contributions. Second, participants contribute additional money to the DC Plan as an after-tax contribution up to the annual additions limit ($56,000 for 2019). Third, participants convert their after-tax contribution into a Roth account in the same year they paid taxes on their after-tax contributions (i.e., an “In-plan Roth Conversion”).

The earnings under a Roth account are tax-free for “qualified distributions” (e.g., distributions after the participant has attained age 59-1/2 and the amounts have been in the DC Plan for at least five years). By contrast, the earnings on after-tax contributions not converted into a Roth account are taxed when distributed from the DC Plan.

Technical Considerations

- Federal Tax Treatment. In an In-plan Roth Conversion, money never actually leaves the DC Plan; instead, it is transferred from the participant’s after-tax contribution account to his or her In-plan Roth Conversion account. For Federal income tax purposes, the conversion amount is treated as if it was distributed from the DC Plan and then immediately recontributed by the participant to the DC Plan.

- Withholding. There is no withholding on the amount converted to pay any resulting income taxes. So, the participant must pay relevant taxes from sources outside of the DC Plan.

- No Early Withdrawal Penalty. Participants under age 59-1/2 who elect an In-plan Roth Conversion are not subject to the 10% additional income tax that would normally apply to a pre-age 59-1/2 distribution from the DC Plan.

- Five-Year Holding Period. Each In-plan Roth Conversion has a new five-year clock attached to it in order to be considered a “qualified distribution.” So, for example, if a participant were to convert after-tax money on December 31, 2020, the clock would expire December 31, 2025, and any distributions of those monies after that date would be considered a qualified distribution. If a participant were to subsequently convert after-tax money on December 31, 2021, that money would have a new five-year clock, expiring December 31, 2026.

- Non-discrimination Testing. After-tax contributions are subject to the actual contribution percentage (ACP) nondiscrimination test. The ACP test compares the average contribution percentages (after-tax contributions and company match, if any) of highly compensated employees (HCEs) and non-highly compensated employees (NHCEs). The ACP of HCEs may not exceed the ACP of NHCEs by more than the legal limit. Note that although a safe harbor 401(k) plan automatically satisfies the ACP test, after-tax contributions are nevertheless required to be tested and may be combined with matching contributions for this purpose. If the DC Plan fails the ACP test, then the after-tax contributions of the HCEs must be limited and any discriminatory excess contributions refunded to HCEs. A plan sponsor can minimize the risk of failing the ACP test by modeling the test in advance and capping after-tax contributions as necessary.

Tax Considerations for Earnings on In-plan Roth Conversions of After-Tax Contributions

An In-plan Roth Conversion of after-tax contributions before any earnings on those contributions have been credited to the participant’s account (i.e., in the same year that the after-tax contributions are made to the DC Plan) will not have any income resulting from the conversion and will be treated as converting only after-tax contributions. Conversely, an In-plan Roth Conversion from after-tax contributions after earnings on those contributions have been credited to the participant’s account (i.e., in any year after the year the after-tax contributions are made to the DC Plan) will result in immediate income to the participant of the earnings.

So, what is the takeaway? All subsequent investment earnings on an In-plan Roth Conversion of after-tax contributions, whether before or after earnings on those contributions have been credited to the participant’s account, will grow tax-free if left in the DC Plan for at least 5 years and withdrawn after the participant attains age 59-1/2. This strategy can be a boon for executives who have the resources but no savings vehicle.

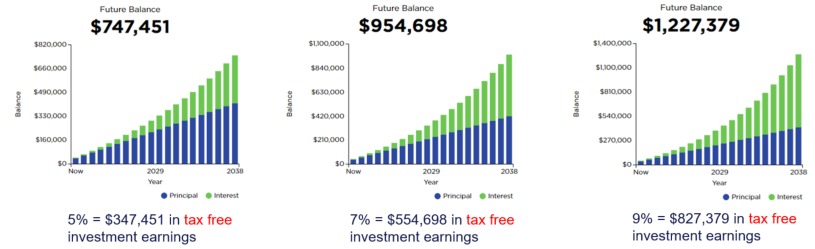

Earnings Examples:

What are the potential tax-free investment earnings on a one-time $20,000 In-plan Roth Conversion at 5%, 7% and 9% interest rates over 20 years?

What are the potential tax-free investment earnings on annual In-plan Roth Conversions at 5%, 7% and 9% interest rates over 20 years?

Next Steps for Plan Sponsors

- Run the ACP test to see if the HCEs have room to make additional after-tax contributions.

- Obtain corporate governance approvals.

- Amend the DC Plan document.

- Prepare participant communications and on-site presentations for educating participants about the new DC Plan feature.

- Work with the DC Plan recordkeeper to conduct mid-year ACP forecasting in the year of implementation.

If you have questions about the In-plan Roth Conversion feature, or you want to add the In-plan Roth Conversion feature to your defined contribution plan, please contact an attorney in our Employee Benefits and Executive Compensation Practice.