Articles + Publications June 22, 2023

Recent Tax Court Case Supports Expansive Reading of Service Condition Requirement and Tiered Partnership Structures for Profits Interests

On May 3, the U.S. Tax Court issued a ruling in ES NPA Holding, LLC v. Comm’r of Internal Revenue, T.C.M. (RIA) 2023-055 (T.C. 2023) in favor of the taxpayer petitioner, holding that the limited liability company interest received by the taxpayer constituted a “profits interest” under Revenue Procedure 93-27, 1993-2 C.B. 343 (Rev. Prov. 93-27). In holding for the taxpayer, the Tax Court took an expansive view of the nature of services required to be provided “to or for the benefit” of the issuing partnership to qualify as a profits interest under Rev. Proc. 93-27. The Tax Court’s holding provides support for the common market practice of issuing profits interests through a “tiered partnership” structure, whereby individual service providers are granted partnership interests in an aggregator partnership vehicle, which interests directly track the economics of partnership profits interests in the service recipient issued to the aggregator partnership vehicle.

Tiered partnership structures are often favored by companies, despite the added administrative costs of establishing and maintaining an additional partnership vehicle because they (1) allow for employee-specific incentive equity provisions (e.g., vesting, forfeiture, and repurchase rights) to be addressed in a separate employee-only vehicle; (2) permit an issuer more control over information rights at the investment partnership level; and (3) could mitigate issues that may arise in certain structures because an individual service provider cannot be treated as an employee for tax purposes of an entity in which the service provider is a partner or in any subsidiary that is a disregarded entity.

Background

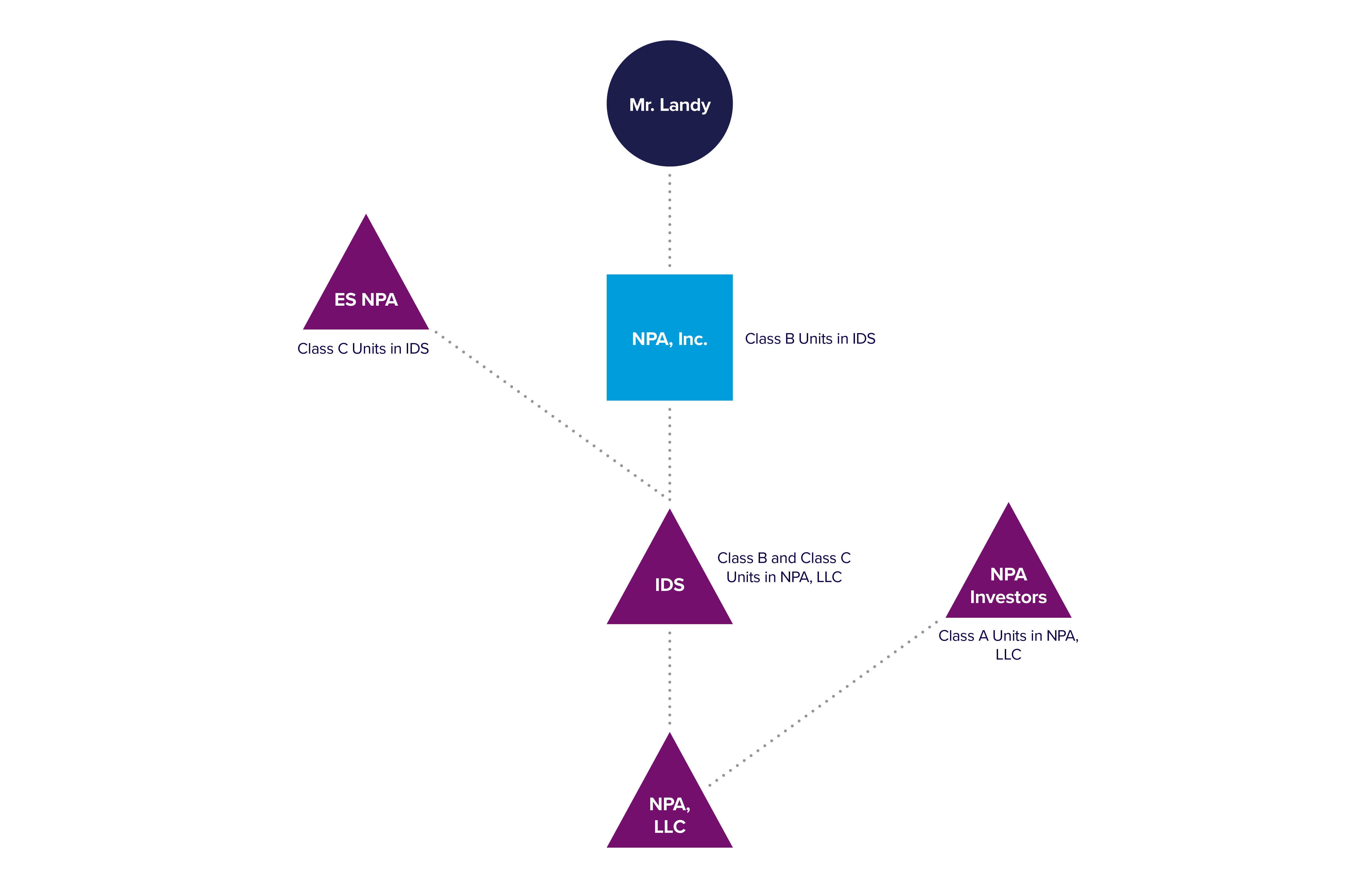

Josh Landy owned 100% of National Processing of America, Inc. (NPA, Inc.) and various other entities involved in the consumer loan business. To facilitate the sale of a portion of the business, NPA, Inc. formed two wholly owned LLCs, Integrated Development Solutions, LLC (IDS) and National Performance Agency, LLC (NPA, LLC). IDS had two classes of membership units, class B and class C. NPA, LLC had three classes of membership units, class A, class B, and class C. The class B and C membership units of IDS tracked the class B and class C membership units of NPA, LLC. NPA, Inc. contributed substantially all of its business assets to NPA, LLC in exchange for all three classes of units (A, B and C). NPA, Inc. then contributed all three class of units of NPA, LLC to IDS. NPA Investors LP (NPA Investors) acquired all of NPA, LLC’s class A units from IDS for a purchase price of $20,985,509 on October 14, 2011.[1] Also on October 14, 2011, ES NPA Holding, LLC (ES NPA), an affiliate of NPA Investors, exercised a call option granted to it by NPA, Inc. to acquire all of the class C units of IDS from NPA, Inc., which class C units reflected an indirect interest in the class C units of NPA, LLC, for payment of $100,000 and the provision of “strategic advice for the purpose of enhancing the performance of [NPA, Inc.’s] business.”

Following the transactions, (1) NPA Investors, through its ownership of the class A units, was entitled to 40% of the liquidation proceeds distributed by NPA, LLC, and had a capital contribution of $20,985,509; (2) NPA, Inc., through its ownership of the IDS class B units, was entitled to 30% of the liquidation proceeds distributed by NPA, LLC, and had a capital contribution of $8,993,790; and (3) ES NPA, through its ownership of the IDS class C units, was entitled to 30% of the liquidation proceeds distributed by NPA, LLC, and had a capital contribution of $0. The class C units were granted to ES NPA in exchange for services to be provided to NPA, Inc., as noted above, and were intended to constitute profits interests under Rev. Proc. 93-27. The class C units were only entitled to share in distributions after all of the capital contributions made by the class A unitholders had been returned to the class A unitholders, with any distributions that otherwise would have been paid to the class C unitholders before such point being paid to the class A unitholders. In other words, the NPA Investors’ purchase price of $20,985,509 for the class A units entitled NPA Investors to a 70% share of NPA, LLC, were NPA, LLC to be liquidated as of the acquisition date.

The following is an illustration of the organizational structure after the transactions:

ES NPA contended that its indirect receipt of the class C units in NPA, LLC (through ES NPA’s receipt of the class C units in IDS), upon exercise of the call option on October 14, 2011, constituted a profits interest under Rev. Proc. 93-27 and related caselaw that was excludable from income for the tax year ending December 31, 2011. The Internal Revenue Service (IRS), however, argued that Rev. Proc. 93-27 was inapplicable because ES NPA did not provide services to IDS or NPA, LLC.

Taxation of Profits Interests

Under Rev. Proc. 93-27, a “capital interest” is defined as an interest that would “give the holder a share of the proceeds if the partnership’s assets were sold at fair market value and then the proceeds were distributed in a complete liquidation of the partnership” at the time of receipt of the partnership interest.[2] A “profits interest” is defined simply as a partnership interest “other than a capital interest.”[3] In general, the receipt of a capital interest in exchange for services is taxable to the service provider.[4] On the other hand, the IRS provided in Rev. Proc. 93-27 that it will not treat the receipt of a profits interest as a taxable event.[5] To qualify as a profits interest under Rev. Proc. 93-27, among other things, the interest must be granted in exchange for the “provision of services to or for the benefit of a partnership in a partner capacity or in anticipation of being a partner.”[6]

Applicability of Rev. Proc. 93-27

In ES NPA Holding, LLC, the IRS argued that Rev. Proc. 93-27 did not apply because Rev. Proc. 93-27 is merely a “safe harbor” with limited application, and ES NPA received an interest in IDS in exchange for services it provided to NPA, Inc. — not NPA, LLC. In rejecting the IRS’s contention, the Tax Court found the IRS’s reading of Rev. Proc. 93-27 to be “unreasonably narrow,”[7] citing a federal tax treatise for the proposition that Rev. Proc. 93-27 is “a ‘broad, taxpayer-friendly safe harbor’ subject only to tightly defined exceptions.”[8]

The Tax Court held that Rev. Proc. 93-27 was applicable to ES NPA’s receipt of class C units in IDS because the material assets of the partnership were held in NPA, LLC, and the activities ES NPA performed were to and for the benefit of the future partnership. The Tax Court went on to opine that “[i]t is of no material consequence that ES NPA’s interest in NPA, LLC is held indirectly through IDS, which is a mere conduit since the liquidation rights in the class C units in both IDS and NPA, LLC are identical.”[9] The Tax Court took a holistic view of the overall partnership structure, pointing out that the partnership came about “only through ES NPA and NPA, Inc.’s joint ownership of IDS and their ownership interest in NPA, LLC.”[10]

In finding that the receipt of the class C units qualifies under Rev. Proc. 93-27, the Tax Court next looked to see if ES NPA satisfied the requirements of Rev. Proc. 93-27, and noted that it must examine whether ES NPA would receive a distribution upon a hypothetical liquidation at the time of receipt. The IRS introduced expert witness testimony, arguing that the sale undervalued NPA, LLC and that the $20,985,509 purchase price paid to acquire the class A units constituted a 40% interest as opposed to a 70% interest in the partnership, thereby implying an overall value of the partnership of $52,463,722 and a liquidation value of $12,169,000 for the class C units at grant. The Tax Court rejected this approach, finding that the transaction was a bona fide arm’s length transaction and held that such a transaction is the best method for valuing an interest before reiterating the view that a bona fide arm’s length transaction is the best method for valuing illiquid securities. Based on the arm’s length purchase price, the Tax Court concluded that ES NPA would not receive a share of the proceeds upon a hypothetical liquidation of NPA, LLC, and ES NPA met the requirement of Rev. Proc. 93-27. This issue highlights the importance of obtaining accurate and defensible valuations in connection with the grant of profits interests.

Impact on Partnership Profits Interests

The Tax Court’s ruling buttresses the position of an expansive, broad reading of Rev. Proc. 93-27; however, questions remain. The class C units held by ES NPA in IDS completely tracked IDS’s class C units in NPA, LLC. It is not clear how far the concept of “to or for the benefit of” extends in cases where interests do not identically track each other or where there is no explicit tracking but instead a high degree of correlation between the value of interests in one entity and another. In addition, the Tax Court noted that the material assets of the partnership were contained in NPA, LLC, but it remains an open question of whether a different conclusion would be found if NPA, LLC held a smaller portion of the partnership assets. Nevertheless, the Tax Court’s ruling provides much welcome support for the common market practice of issuing profits interests as tracking interests through a “tiered partnership” structure and provides a basis for further analysis to clarify that threshold.

For additional information, please contact any of the attorneys listed in this advisory.

[1] The Tax Court ruling is not entirely clear on all the facts surrounding the purchase; however, it states that NPA Investors paid $14,502,436 for “good will” and $6,483,073 for the existing book of loans for a total purchase price of $20,985,509.

[2] Rev. Proc. 93-27 §2.01.

[3] Id. §2.02.

[4] See, e.g., Crescent Holdings, LLC v. Commissioner, 141 T.C. 477, 488 (2013), Internal Revenue Code §83(a) and Treas. Reg. §1.61-2(d).

[5] The Tax Court focused its analysis on Rev. Proc. 93-27, although it did note that it held in both Diamond v. Commissioner, 56 T.C. 530 (1971), aff’d, 492 F.2d 286 (7th Cir. 1974) and Campbell v. Commissioner, T.C. Memo. 1990-162, aff’d in part, rev’d in part, 943 F.2d 815 (8th Cir. 1991) that the receipt of a partnership profits interest in exchange for the performance of services was a taxable event before the U.S. Court of Appeals for the Eight Circuit reversed the Tax Court’s decision in Campbell. ES NPA Holding, LLC is appealable to the Eighth Circuit, and the Tax Court left unanswered the question of how its rulings in Diamond and Campbell would have impacted its decision were the case appealable to a different circuit court.

[6] Id §4.01. Revenue Procedure 2001-43, §2, 2001-2 C.B. at 191 further clarified that the determination of whether an interest is a profits interest is tested at the time of grant.

[7] See, ES NPA Holding, LLC at 11.

[8] Id at 12 citing William S. McKee et al., Federal Taxation of Partnerships and Partners ¶ 5.02[2] (2022).

[9] Id at 12.

[10] Id. at 12.

Insight Industries + Practices

Speaking Engagements

Massachusetts Collectors and Treasurers Association: 55th Annual School

August 11 – 14, 2026

University of Massachusetts Amherst

91 Campus Center Way, Amherst, MA 01003

Speaking Engagements

Private Equity in Healthcare: How Sick Is The Patient?

August 4, 2026 | 12:00 PM – 1:15 PM ET

Annapolis Waterfront Hotel

80 Compromise Street, Annapolis, MD 21401

Speaking Engagements

2026 ACI Women Leaders in Life Sciences Law

July 29 – 30, 2026

Seaport Hotel Boston

1 Seaport Ln, Boston, MA 02210

Speaking Engagements

72nd Annual Natural Resources and Energy Law Institute

July 24, 2026 | 4:30 PM – 5:30 PM PT

Seattle, WA